Related Flashcards

Related Topics

Cards In This Set

| Front | Back |

|

2 Relevant costs and revenues What are relevant costs?

|

2 Relevant costs and revenues Relevant costs are future cash flows arising as a direct consequence of the

decision under consideration

|

|

2 Relevant costs and revenues What are the three elements to relevant costs and revenues?

|

2 Relevant costs and revenues 1) Cash flows. Actual cash flows should be

considered. Noncash items such as depreciation and interdivisional charges

should be ignored. 2) Future costs and revenues. Past costs and revenues are

only useful as a guide to the future. Costs already spent - sunk costs- are irrelevant for decision making. 3) Differential costs and

revenues. Only the costs and revenues that alter as a result of a

decision are relevant. Factors common to all alternatives being

considered can be ignored; only the differences are relevant.

|

|

2 Relevant costs and revenues 1) Things to consider is shortrun situations 2) Things to consider in the longrun

|

2 Relevant costs and revenues 1) In many shortrun situations fixed costs remain constant for each alternatives being considered therefore marginal costing showing

sales, marginal cost and contribution is particularly appropriate 2) Fixed costs do change and the differential costs must include any

changes in the amount of fixed costs.

|

|

3 Opportunity cost What is opportunity cost?

|

- Value of the best alternative that is foregone when a particular

course of action is undertaken. - by choosing one plan there may well be sacrifices elsewhere in

the business.

|

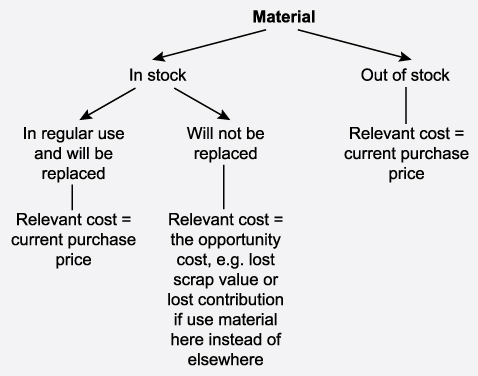

4 The relevant cost of materials |

4 The relevant cost of materials |

|

4 The relevant cost of materials Are historic materials cost relevant?

|

4 The relevant cost of materials - always a sunk cost and never relevant unless

it happens to be the same as the current purchase price.

|

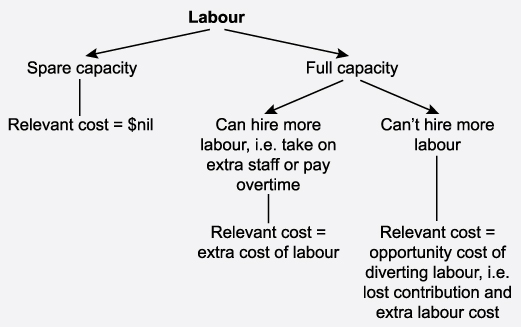

5 The relevant cost of labour |

5 The relevant cost of labour |

|

6 Make versus buy When should a product be made in house?

|

6 Make versus buy - if relevant cost of making the product in-house is less than the cost of

buying the product externally.

|

|

6 Make versus buy If spare capacity exists, what is the relevant cost of making the product in-house?

|

6 Make versus buy relevant cost = variable cost of internal

manufacture + fixed costs directly related to that product

|

|

6 Make versus buy If no spare capacity exists, what is the relevant cost of making the product in-house?

|

6 Make versus buy relevant cost = variable cost of internal manufacture + fixed

costs directly related to that product + opportunity cost of internal

manufacture (e.g. lost contribution from another product).

|

|

6 Make versus buy In addition to the relative

cost of buying externally compared to making in-house, whatother issues must also be considered?

|

Reliability of external supplier- quantity required- quality required- delivering on time- price stability Specialist skills: the external supplier may possess some

specialist skills that are not available in-house Alternative use of resource: outsourcing will free up resources

which may be used in another part of the business. Social: will outsourcing result in a reduction of the

workforce? Redundancy costs should be considered. Legal: will outsourcing affect contractual obligations with

suppliers or employees? Confidentiality: is there a risk of loss of confidentiality,

especially if the external supplier performs similar work for rival companies Customer reaction: Do customers attach importance to the

products being made in-house?

|

|

7 Shut-down decisions When considering the quantifiable cost or benefit of closure, what relevant cash flows associated with closure should be considered?

|

7 Shut-down decisions - the lost contribution from the area that is being closed (= relevant cost of

closure) - savings in specific fixed costs from closure (=relevant benefit of closure) - known penalties and other costs resulting from the closure, e.g. redundancy,

compensation to customers (=relevant cost of closure) - any known reorganisation costs (= relevant cost of closure) - any known additional contribution from the alternative use for resources

released (= relevant benefit of closure)

|

|

7 Shut-down decisions What are the non-quantifiable costs and benefits of

closure

|

7 Shut-down decisions - penalties and other costs resulting from the closure (e.g. redundancy,

compensation to customers) may not be known with certainty. - reorganisation costs may not be known with certainty - additional contribution from the alternative use for resources released may not

be known with certainty - Knock-on impact of the shut-down decision. For example, supermarkets often

stock some goods which they sell at a loss. This is to get customers through the

door, who they then hope will purchase other products which have higher profit

margins for them. If the decision is taken to stop selling these products then

the customers may no longer come to the store

|

|

8 One-off contracts When a business is presented

with a one-off contract how should it calculate the The minimum contract price? When should the contract be rejected?

|

8 One-off contracts The minimum contract price = the total of the relevant cash flows associated with the contract. If the contract price does not cover these cash flows then it should be rejected

|

|

9 Further processing decisions When deciding whether to

process a product further or to sell after split-off which future incremental

cash flows should be considered?

|

9 Further processing decisions - Any difference in revenue and any extra costs - Joint costs are sunk at this stage and thus not relevant to the decision

|